Why Invest in Vacation Properties: 2026 Investor Guide

- info67421305

- May 25

- 9 min read

TL;DR:

Vacation properties are lifestyle-focused assets with income potential, but they involve significant operational demands and risks.

Choosing stable markets with regulatory certainty and active management is key to maintaining reliable occupancy and profitability.

If you’re weighing vacation property investment against other real estate options, the honest answer isn’t straightforward. Knowing why invest in vacation properties matters before you commit capital is the difference between a smart diversification move and a costly lifestyle purchase you’ve dressed up as a financial strategy. The data shows real income potential exists, but so do real risks: occupancy volatility, regulatory shifts, and operational demands that most buyers don’t anticipate. This guide cuts through the enthusiasm and gives you a grounded look at what vacation rental investing actually delivers.

Table of Contents

Key takeaways

Point | Details |

Vacation properties are lifestyle-first assets | Treat them as lifestyle investments with income upside, not guaranteed cash machines. |

Location and regulation drive returns | Markets with stable rules and supply constraints produce the most reliable rental income. |

Operations require active involvement | Short-term rentals demand dynamic pricing, guest management, and maintenance that long-term rentals do not. |

Tax benefits are conditional | Accelerated depreciation and deductions require material participation and professional record keeping. |

Management partners change outcomes | Vancouver Airbnb owners who use professional property managers consistently outperform self-managed properties. |

Why invest in vacation properties: the financial fundamentals

Before anything else, let’s talk numbers. Vacation property investment carries a specific cost profile that many buyers underestimate until they’re six months in.

The upfront costs are obvious: purchase price, closing fees, inspections, and initial furnishing. The ongoing costs are where investors get surprised. Annual maintenance alone typically runs 1 to 4% of property value every year. On a $600,000 property, that’s $6,000 to $24,000 before you’ve paid a mortgage, utility bill, or property tax. Add HOA fees, short-term rental licensing, insurance, and platform fees, and your carrying cost baseline climbs fast.

The income side of the equation is genuinely strong in the right markets. Experienced operators in strong markets net over $62,000 annually per property, though that figure requires active management and market selection discipline. National occupancy averages sit around 48.4%, but revenue is driven by pricing power, not calendar fullness. A property generating $350 per night at 55% occupancy outperforms one charging $180 at 70%.

Here’s the comparison most investors avoid:

Investment vehicle | Avg. annual return | Liquidity | Active management required |

S&P 500 index fund | ~10% | High | None |

Residential vacation rental | 4–8% net | Low | High |

Long-term rental property | 5–7% net | Low | Moderate |

Vacation home (appreciation only) | 3–5% | Low | Low |

Vacation homes historically appreciate at 3 to 5% annually, which trails diversified equity portfolios. The case for vacation rentals isn’t raw return. It’s the combination of rental income, appreciation, personal use value, and tax advantages that makes the total picture compelling for the right investor.

Pro Tip: Budget for hidden costs including re-registration fees, management fees, and platform adjustments. Financial advisors recommend vacation home purchases only when the total cost stays below 20 to 30% of your net worth.

Market dynamics and location factors

Not all vacation markets are equal. The biggest mistake investors make is chasing trending destinations rather than markets with entrenched, generational demand.

Markets with drive-to accessibility and multi-generational tourism histories provide the most resilient income across economic cycles. Think mountain towns that attract skiers in winter and hikers in summer, rather than a beach community that draws crowds for eight weeks and goes quiet after Labor Day.

Mountain tourism markets generate stable, year-round demand and support premium pricing because the experience itself, not just the bed, is what guests pay for. Mountain cabin rentals with recreation access and views regularly command nightly rates 40 to 60% above comparable urban properties. Annual occupancy in mountain destinations frequently runs between 70 and 85%, supporting consistent year-round income.

Compare two hypothetical markets:

Market type | Peak occupancy | Off-season occupancy | Avg. ADR | Regulatory stability |

Mountain resort town | 90%+ | 65–75% | $320/night | High (zoning limits supply) |

Urban coastal city | 80%+ | 30–40% | $210/night | Low (frequent rule changes) |

The regulatory environment matters as much as demand. Stable regulatory frameworks correlate directly with investor confidence and long-term property values. Markets that cap short-term rental supply through zoning or licensing create natural pricing floors. Markets that flip between permissive and restrictive rules every election cycle destroy investor confidence and suppress values.

Pro Tip: Before purchasing, verify HOA rules and municipal short-term rental ordinances. Many neighborhoods in cities like Scottsdale restrict rentals at the HOA level, a fact buyers routinely miss until after closing.

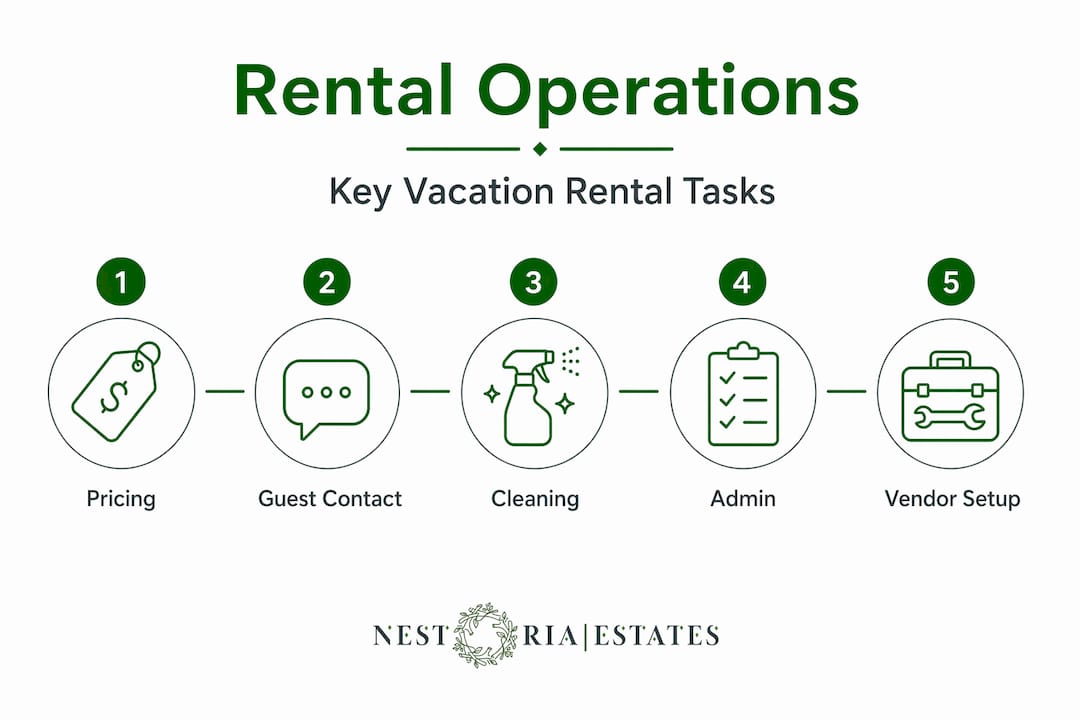

Operational demands of vacation rentals

Here’s where the “passive income” narrative falls apart for most buyers. Short-term vacation rentals are not passive. They are hospitality businesses that happen to be operated from your phone.

The operational load includes dynamic pricing management, guest communication before and during stays, cleaning coordination between bookings, restocking, maintenance calls, and review management. Unlike long-term rentals where you collect rent and respond to occasional repair requests, vacation rentals require weekly or daily attention.

The income premium reflects that reality. Net income premiums of 20 to 40% over long-term rentals are achievable, but only with active management. Investors who treat vacation rentals as hospitality businesses, not just real estate holdings, are the ones hitting those numbers.

Administrative failures are a specific and underappreciated risk. 27% of vacation property cases in recent studies incurred penalty fees or utility disruptions due to missed re-registration deadlines. These aren’t catastrophic events. They’re slow drains on returns that compound over time. You can learn more about common yield mistakes that silently reduce profitability.

For Vancouver Airbnb owners specifically, local vendor infrastructure is the deciding factor in remote investment success. Lack of reliable vendor networks leads to operational failures even in high-demand markets. Having dependable cleaners, repair contractors, and a management firm you trust isn’t a luxury. It’s what determines whether your rental runs like a business or like a headache.

Pro Tip: Dynamic pricing adjusted manually on a weekly basis consistently outperforms default platform algorithms. If you’re not repricing based on local events, competitor inventory, and booking pace, you’re leaving real money on the table.

Tax implications for vacation property investors

The tax side of vacation property investment is genuinely attractive, but only if you understand the rules upfront.

The 14-day personal use rule. The Tax Cuts and Jobs Act limits your ability to deduct rental losses if you personally use the property for more than 14 days per year or more than 10% of the days it’s rented. Cross that threshold and the IRS classifies it as a personal residence, not a rental. Loss deductions disappear.

Material participation requirements. To unlock the full tax benefit of short-term rentals, including the ability to deduct losses against ordinary income, you must materially participate in operations. That means logging hours and maintaining documentation.

Accelerated depreciation through cost segregation. Tax benefits including accelerated depreciation require professional cost segregation studies. This isn’t a DIY exercise. An accountant who specializes in real estate can reclassify components of your property for faster depreciation, generating significant first-year paper losses.

Record keeping is non-negotiable. Passive loss classifications limit your offset opportunities if participation is poorly documented. Keep a contemporaneous log of management hours and activities.

Vacation home vs. investment property. If you plan to use your property personally and rent it out, be deliberate about which category it falls into. Mixed-use properties require proportional allocation of expenses, which reduces your deductible amounts.

The short-term rental tax strategy can generate major year-one deductions when structured correctly. Done wrong, it provides almost no benefit. Review these advantages of owning vacation rentals from a tax and income perspective before finalizing your approach.

Practical advice for Vancouver Airbnb owners

Vancouver Airbnb owners considering adding a vacation property to their portfolio face a specific set of considerations tied to British Columbia’s regulatory environment and Canada’s tax framework. Here’s how to approach the decision with discipline:

Set an affordability ceiling. The total purchase cost, including mortgage, carrying costs, and management fees, should stay within 20 to 30% of your liquid net worth. For investors with $500,000 to $2,000,000 in liquid assets, this is the range where a vacation property adds portfolio value without creating cash flow pressure.

Choose markets with proven demand. Drive-to markets with multi-season appeal and stable rental regulations outperform trend-driven coastal markets. Ask what the off-season occupancy rate looks like before you commit to any market.

Be honest about personal use. If you plan to use the property for extended personal stays, model it as a lifestyle asset with rental income upside, not a pure investment. The math changes significantly once you start blocking your peak weeks.

Budget for operations from day one. Account for management fees (typically 20 to 30% of gross revenue), cleaning, maintenance, and platform costs before projecting net income. Most investor projections fail because they start from gross revenue and forget operational overhead.

Engage local property management expertise early. Local vendor infrastructure is the deciding factor in whether remote investment works. A credible local property management firm reduces operational risk and improves guest experience, which directly drives reviews and repeat bookings.

Evaluate opportunity cost. Before committing capital, compare projected vacation rental returns against what the same capital would generate in a diversified portfolio. The gap is real. The advantages of vacation rentals, including personal use and tax efficiency, need to close that gap for the investment to make sense.

Pro Tip: Look at Florida’s vacation rental market as a benchmark for understanding what sustained demand, infrastructure, and regulatory stability actually look like in a mature vacation rental market.

My honest take on vacation property investing

I’ve worked with a lot of vacation property owners over the years, and the pattern I see most clearly is this: the investors who win treat these properties as businesses first and real estate second. They research markets obsessively, they build reliable local teams before they purchase, and they set income projections conservatively rather than working backward from a number they want to be true.

What I find troubling is how many buyers enter vacation property investment purely on appreciation narratives. They buy in a trendy market, assume the property will appreciate 10% annually, and barely mention rental income in their model. That’s not investing. That’s speculating with a mortgage.

The honest case for vacation rental investment is more nuanced than the enthusiasm in most investor forums. Yes, strong operators in the right markets net impressive annual income. Yes, the tax advantages are real when properly structured. And yes, having a property you can also use personally has genuine lifestyle value that doesn’t show up in a spreadsheet. But the returns on a standalone financial basis rarely justify the illiquidity, the operational complexity, and the concentration risk you’re accepting.

Where I’ve seen the clearest wins is with Vancouver Airbnb owners who already understand short-term rental operations. They know what dynamic pricing looks like in practice. They know how reviews drive occupancy. They know the regulatory risk is real. When those owners expand into a second property in a well-chosen market with a management partner they trust, that’s where vacation property investment performs at its best.

— Kamran

How Nestoriaestates can support your vacation property goals

If you’re seriously considering vacation property investment, the operational complexity is real, but it doesn’t have to land on your plate.

Nestoriaestates provides full-service vacation rental management for property owners across Canada and the United States, with deep expertise serving Vancouver Airbnb owners specifically. From dynamic pricing and guest communication to cleaning coordination and maintenance oversight, the team handles every operational detail while you track performance through transparent owner reporting. Whether you’re assessing a new vacation property purchase or improving returns on a property you already own, Nestoriaestates offers free revenue projections and personalized guidance. Reach out directly to talk through your situation with someone who knows the market.

FAQ

Why invest in vacation properties instead of long-term rentals?

Vacation rentals can generate 20 to 40% higher net income than long-term rentals in the right markets, with additional tax benefits and personal use flexibility. The trade-off is significantly higher operational involvement and occupancy variability.

What financial returns can vacation properties realistically deliver?

Experienced operators in strong markets net over $62,000 annually per property, but average returns depend heavily on location, pricing discipline, and management quality. Appreciation historically adds 3 to 5% annually on top of rental income.

How do taxes work for vacation property investors?

Short-term rental tax benefits, including accelerated depreciation, require material participation and professional cost segregation. Personal use exceeding 14 days per year or 10% of rental days limits deductible losses under current IRS rules.

What markets should Vancouver Airbnb owners consider for vacation property investment?

Markets with year-round demand, stable rental regulations, and drive-to accessibility consistently outperform trend-driven destinations. Mountain resort towns with supply constraints offer both pricing power and resilient occupancy.

Do I need a property manager for a vacation rental investment?

You don’t need one, but the data strongly favors it. Professional management reduces administrative failures, improves guest experience, and typically generates returns that more than offset management fees, particularly for remote properties.

Recommended

Comments